In March, the U.S. Government implemented a 25 percent tariff on imported steel and a 10 percent tariff on imported aluminum. Those increases affected domestic steel and aluminum as well, and costs increased on all construction products using those materials.

Expansion overpowers high material costs, long lead times

At the same time steel and aluminum costs were rising, demand for those materials also increased. In response, some companies in the construction supply chain changed how they estimated work and materials, and investigated alternative materials. In some instances, steel and aluminum products took longer to procure than they had in the last couple years. As a result, some projects were canceled altogether, when they were no longer financially viable in light of overall construction cost increases. Most recently, there have been some indications that steel and aluminum costs are beginning to stabilize.

Rising Costs

Companies across the construction supply chain experienced steel and aluminum cost increases since March. Brad Robeson, president at Columbus, Neb.-based Behlen Building Systems, says his company paid 35 percent more for steel for its metal building systems this year compared to 2017.

Component manufacturer costs rose as well. Nashville, Tenn.-based Thompson Research Group surveys the entire construction supply chain for a variety of building products, from producer to end user. One of the products it tracks is steel studs, which recorded 10 percent cost increases every month in 2018, January to September.

Fabricators and installers also experienced steel and aluminum cost increases. Kansas City, Mo.-based fabricator A. Zahner Co. paid about 35 percent more for steel in 2018 versus 2017, and 58 percent more for aluminum, says Gary Davis, director of marketing. Pittsburgh-based erector Solid Steel Buildings Inc. incurred three cost increases for metal building systems totaling a 28 percent increase (12 percent in January, 9 percent in March and 7 percent in May), says Michael Masula, CEO.

The ease with which companies in the construction supply chain can pass along cost increases to customers varies. Steve Klessig, vice president of architecture and engineering at Kaukauna, Wis.-based Keller Inc., says, as a design- builder responsible for both the design and construction of projects, it’s difficult for Keller to pass along rapid cost increases to its customers, which included a 30 percent bump in steel costs since January. “After it’s designed, and you go to market and bid, that’s when you’re finding out that your numbers are higher than you anticipated, and it’s not sold yet,” he says. “That’s too late in the game to decide to switch to precast or something else because the building has been designed already. When we have to pass on those increases, that’s when we could hurt the sale of some new jobs. We’re not bidding against other contractors; we’re bidding against a client deciding if they’re going to go ahead with the project or not because of cost.”

Energized Construction

At the same time steel and aluminum costs increased, construction activity grew. Many companies point to generally favorable overall market conditions as supportive of their businesses’ growth.

Solid Steel Buildings had growth across all construction sectors this year, says Masula, including commercial and industrial, as well as oil, gas and manufacturing. “The general economy is basically is the best I’ve seen it since 2005,” he says. “The markets have driven us to do more than triple of what we’ve done in our best year.”

Masula reports his company is scheduling projects for 2019 and 2020 at this time. The abundance of work gives them the flexibility to be selective with projects. “We can’t write contracts fast enough,” he says. “We’re actually at the point where we get to choose our customers.”

Another company that has been growing throughout 2018 is Chandler, Ariz.-based Kovach Building Enclosures, a national building envelope fabricator and installer. James Hatch, vice president of preconstruction at Kovach, says they’ve seen more private and speculative projects such as office buildings and hotels than in the last few years. “We attribute that to pent-up projects since the last downturn and people just sitting on the sidelines,” he says. “They finally see a ray of hope, this job that’s been on the shelf for eight years, they can now dust it off and strike now while the iron is hot and get it rolling.”

Structural steel fabricators have also experienced growth amid rising steel costs, says Tabitha Stine, SE, PE, LEED AP, vice president at American Institute of Steel Construction (AISC). “The health of the market has been very strong because there’s been a dominance of construction the last two years, which has really led to the health of the domestic fabricator,” she says. “Construction volume in general is probably going to be up about 3 percent in square footage over last year.”

Stine says demand for construction has outweighed overall construction cost increases in 2018. “In construction in general, the prices have gone up, which has caused another kind of concern, but I wouldn’t attribute that solely to the tariff; it’s also supply and demand,” she says. “There’s a demand for more construction, which has allowed the fabricators to be a little bit more busy than usual. Overall, they’ve been healthy.”

Macroeconomic forces help explain why construction activity accelerated at the same time steel and aluminum costs—among other materials—increased, says Anirban Basu, chief economist at Associated Builders and Contractors (ABC). “One reason is sheer big picture, and that’s a picture of a world that is flush with liquidity,” Basu says. “Central banks have been expanding money supply for years following the shared global financial crisis. They have been seeking to restore asset prices as well as economic growth. While the Federal Reserve has been tightening monetary policy, there remain many central banks around the world that continue to supply enormous amounts of new liquidity to the global financial system. That money has got to go somewhere, and people have a tendency to not to want to simply sit on it and generate low rates of interest; they want to deploy that capital.”

Basu also says global capital has continued to flow to America, in part, to avoid more challenging circumstances in other countries including China, South Africa, Turkey, Venezuela, Russia and Brazil. “Another big, macroeconomic point here is that, at least arguably, America has been the best game in town for years,” he says. “This is one of the reasons that the stock market has done so well and people have continued to hold onto U.S. dollar-denominated bonds. A lot of that money has been invested in real estate, and the effect of that has been to bolster the value of hotels, office buildings, shopping centers and other elements of the built environment. That increase in valuation has prompted more construction. So, yes, costs are up, but the appetite to deploy capital aggressively is still very much in place. The presumption is in a quite strong economy that those costs can be recovered at the backend through higher rents or other charges to users. Given the uncertain direction of materials prices and tariff policy, I don’t think that the tariffs are causing people to move forward with projects; I think people are moving forward with projects despite the tariffs and other sources of cost increase.”

Material Costs Rising Faster than Bid Prices, Source: U.S. Bureau of Labor Statistics, courtesy of AGC

Click on chart to enlarge.

Click on chart to enlarge.

Caption: The producer price index (PPI) for new nonresidential building construction, or bid prices (black line), increased 5 percent from October 2017 to October 2018. Before turning higher in October, the year-over-year change was around 3 to 4 percent each month between mid-2017 and September 2018.

The PPI for construction inputs (blue line) shows the year-over-year change in the cost of materials and services used in every type of construction. It increased 6.6 percent from October 2017 to October 2018. The year-over-year change was consistently larger than the change in bid prices each month between mid-2017 and September 2018.

The year-over-year change in wages and salaries (average hourly earnings) for all construction employees (red line) increased 3.8 percent from October 2017 to October 2018. The year-over-year change was about 3 percent each month between mid-2017 and September 2018, close to the rate of change in bid prices.

Kenneth Simonson, chief economist at Associated General Contractors of America, says, “In short, since mid-2017 contractors have been raising their bid prices at a rate that roughly matches the increase in their payroll costs but have not kept up with fast-rising materials costs.”

Revised Estimates

The most difficult task in construction today is estimating because estimators are the ones that have to predict material and labor costs accurately in order to ensure profitability, Basu says. “The challenges estimators face are enormous because there’s been a scramble for domestic steel, and many construction firms have told me their steel supplier tells them that we can’t guarantee supply in six months or nine months. And so you put all that together and the estimator is really struggling to figure all these things out, and the stakes are enormous.”

Hatch says Kovach changed its estimating process to accommodate rapidly rising steel and aluminum costs. Beginning in January, some of its steel and aluminum vendors changed their estimate validity periods from 30 days to 24 hours, and notified Kovach to anticipate 15- to 20-percent price increases after a period of time. “Beyond 24 hours, we’d have to get it re-quoted, which really doesn’t help us much,” Hatch says. “We need to have a window to submit our bid and get a contract, so that was a challenge.”

Kovach responded to the pricing volatility by decreasing its estimate validity period for customers from 60 days to 15 days. “Basically, we had to draw a line in the sand,” Hatch says. “Previously we had felt comfortable with our number and having some type of buffer in our bid so if there’s a minor increase, it doesn’t really affect where we’re at. But it really shifted our willingness to be flexible on that.”

Basu says the willingness of contractors to guarantee their estimates can become another basis for competition. “If I’m a general contractor, I’m going to probably choose the firm, all things being equal, who is able to guarantee their price the longest,” he says. “And that’s the firm who’s willing to take the greatest amount of risk on a shifting global economy and shifting global economic policies. It used to be that people would compete on price and construction time, but now they also compete on whether or not there are contingencies in the contract.”

Creative Engineering

Higher steel and aluminum costs have make other materials more competitive, and, as Basu points out, prompt designers to reconsider specifying those metals. According to Basu in the last six months tariffs have pressured architects and engineers to reengineer projects and find replacement materials to minimize the impacts of the tariffs. “I don’t think we would call that value engineering. That’s a different proposition. But I think what we would call that is creative engineering to try to get around these trade policy-induced impacts.”

In one example of design reevaluation, Russ Sanders, AIA, principal and workplace studio leader at SmithGroup in Phoenix, says he’s been working on an airport terminal in which they’ve completed studies evaluating the use of steel versus concrete. In a previous project at the same airport, concrete was used for the apron, and then it transitions to steel at the passenger level and roof structure. For the current project, the steel is likely to be decreased and the concrete increased, so the concrete continues up to the roof, Sanders says. “I don’t know how much of that is cost driven, but I suspect some of it is cost driven because we are hearing that steel escalation is going up.”

Sanders says SmithGroup is conducting additional design evaluations to control costs for other projects, as well. “[The increased steel prices are] causing us to not necessarily go directly to steel as we might have in the past,” he says. “We’re in a position now where we have to question everything because what’s happening with steel has caused us to not assume anymore, but do additional evaluations of structural systems that we might not have had to do a year ago.”

Photo courtesy of AISC

Delayed and Canceled Jobs

Increased overall construction cost was a factor in the financial practicality of several projects Seattlebased BuildingWork LLC has been working on in the last six months. Matt Aalfs, AIA, principal at BuildingWork, says construction of two renovation projects with significant amounts of steel and aluminum were put on hold indefinitely.

“We’re really facing a tipping point in construction costs with our projects,” Aalfs says. “We had completely designed them and were ready to start construction, but they’re not going forward because construction costs are too high, so they’re not financially viable for the developer.”

Another one of the firm’s renovation projects is being delayed as steel and other costs are being reevaluated, Aalfs says “[The project is] teetering on whether it will proceed. The developer is working with the general contractor to find a way to get the construction costs down so that the project has the financial viability for the investment group to decide to build it.”

A single project being delayed or canceled due to construction costs can have a significant impact on his relatively small firm, Aalfs says, which completes many medium size building projects. And the medium sized projects are also less able to absorb cost increases, he says. “The very large projects can absorb some costs and still be financially viable, but it’s these small to medium size projects that don’t have the financial elasticity from the developer’s perspective to be able to absorb significant increased costs. Whether they’re new construction or renovation, the financial model is already very tight. Any significant increase can tip the project into no longer being viable, and that has a significant impact on us because we may have been counting on that revenue stream, but it isn’t going to happen.”

Long Lead Times

Procurement lead times for steel and aluminum and their impacts on companies across the construction supply chain varied by material, geography, place in the supply chain, timing and other factors. For a renovation project BuildingWork designed with a large amount of structural steel, construction has been delayed due to the steel, Aalfs says. “The contractor is looking at weeks of delay over what they had expected in order to find and get the steel delivered and fabricated. I don’t know exactly how much of this is related directly to the tariffs, but definitely the increase in steel costs and the delay in procurement of steel is something that is impacting us quite a bit.”

Stine says when the tariffs started in March, steel fabricators had to purchase from more than one service center. There was uncertainty and risk for the service centers to carry a lot in stock, and the mill cycles were a little longer, she says. “In the last two and half months, I haven’t heard of that being an issue. It’s kind of relaxed; there was a lot of pent up nervousness and now we’re starting to see more of a traditional way of ordering material like we saw a year ago.”

For Kovach’s orders of aluminum extrusions for curtainwall framing, metal rainscreen panel supports, trim pieces and other components, Hatch says typical lead times dramatically increased in the last six months. “Lead times have been almost a bigger problem for us than the price,” he says. “We’ve seen lead times almost double in certain products that we’re supplied; where it was once at eight weeks, it’s now pushing 18 weeks.”

The change in lead times for materials has required Kovach to communicate more with customers to manage their expectations, Hatch says. “It’s an interesting climate right now that I think owners are still thinking that they’re operating five years ago, where they expect you can get new material on site in four weeks; but no, you can’t,” he says. “That was the perfect world, and everything had to go great, and now that’s tripled.”

Part of the explanation for why aluminum is taking much longer to procure than steel is that it is produced in a smaller number of places in the world compared to steel, Basu says. “Coming into this era of tariffs on steel and aluminum, there was much more excess capacity amongst steel manufacturers. When the tariffs hit, steel manufacturers had more capacity to turn back on quickly to respond to the market impetus. But aluminum production capacity is much more limited, and capacitation has been higher, so that market has not been as quick to respond.”

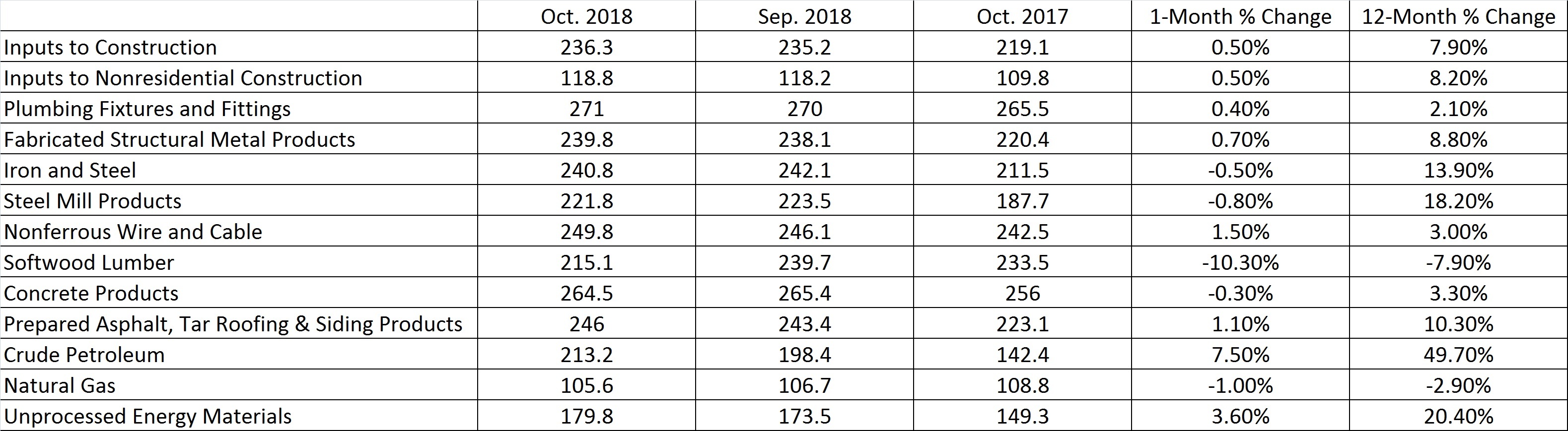

Producer Price Index by Material, October 2018, Source: U.S. Bureau of Labor Statistics, courtesy of ABC

Click on table to enlarge.

Click on table to enlarge.

Signs of Stabilization

After about a year of escalating steel and aluminum costs and concurrent stimulus in construction activity, there are indications that some costs may be stabilizing. Kathryn Thompson, partner and CEO at Thompson Research Group, says after multiple price increases for steel, they are starting to see some abatement. In her firm’s third quarter survey, 56 percent of respondents reported pricing of steel studs was down in the last 30 to 60 days.

“I think what’s consistent in terms of feedback is consumers and distributors are telling us that they feel that the worst is behind them in terms of increases in steel prices in 2018,” Thompson says. “And when you look at hot-roll coil prices, they started to come down in August. They’re still up year over year, but they are back closer to March-type levels.”

Kenneth Simonson, chief economist at Associated General Contractors of America (AGC), says unlike earlier in the year, he has not recently received price increase announcements for steel and aluminum materials. “In fact, the producer price index (PPI) for aluminum mill shapes dipped 0.4 percent from September to October and a total of 2.8 percent from July to October, although it is still 8.2 percent higher than in October 2017, consistent with the 10 percent tariff that was imposed,” he says. “The PPI for steel mill products declined 0.8 for the month of October, but was up 1.8 percent over July and up 18.2 percent from a year ago, also roughly consistent with a partial 25 percent tariff.” Basu says he has also observed softening prices and that increases in supply to meet demand could support that dynamic. “When you look at the producer price index data, which comes from the Bureau of Labor Statistics, over the last two months there are indications that materials prices are no longer rising as they have been in the previous six to eight months,” he says. “One of the things economists like to point out is, a cure for high prices is high prices. And that means that higher prices stimulate production. And so this may have something to do with American producers stepping up because of these higher prices, and expanding their supply. And that will tend to have a moderating impact on prices.”