The strength of individual markets is shifting, and the forecast from FMI for total construction put in place for 2013 continues to show an increase of 8 percent over 2012 levels. The forecast total for construction in 2013 is $918,897 million, a solid improvement, but we don’t expect to return to the days of annual construction above the trillion-dollar mark until 2015. The star of the show is residential buildings with a 23 percent rise in single-family buildings. In the early months of the Great Recession, it seemed that nonresidential construction would manage to hold enough momentum to carry it through even though residential construction was tanking. It might have made it if the recession had been of the brief variety. We are now seeing a lag on the upside as commercial, lodging and office construction finally start to pick up.

Continued low interest rates provide much of the stimulus for the new growth in capital spending, but that hasn’t been enough for many large businesses focused on using their record profits to pay down debt or otherwise strengthen their balance sheets. While much of business is still in wait-and-see mode, some are breaking the mold and planning for growth. Then there is the power industry, oil and gas exploration is booming in the rich shale regions.

These booming regions buck the trends across the nation, with rising labor costs and need for housing and construction of roads, rail and pipelines to move the product from the fields to refining and distribution sites. The potential for greater energy independence and lower energy prices is helping to make the U.S. more competitive in the global market and enticing more manufacturing to relocate in the U.S., and that is not just American companies. While low interest rates, rising material and labor costs as well as the growth in housing sales and construction smack of a coming period of inflation, so far, the consumer price index remains relatively tame. Nonetheless, higher interest rates are inevitable down the road, but most economists don’t expect that to happen this year.

Lodging

After three years of steep declines, the market for lodging construction came back a strong 25 percent in 2012 and we expect another 10 percent growth in construction put in place for 2013 to

$12.2 billion. Lodging’s comeback has been slow as both consumers and businesspeople cut down sharply on travel in the past few years. However, lately, according to STR, “[T]he U.S. hotel industry’s occupancy rose 2.0 percent to 58.5 percent, its average daily rate was up 4.4 percent to US$107.72, and its revenue per available room increased 6.4 percent to US$63.04.” (Reported in www.hotelnewsnow.com/Articles.aspx/10087/ STR-reports-US-hotel-pipeline-for-February)

The sharp drop in construction of new properties has helped to keep the rates high, but now the lodging industry is looking at a longer-term plan to add rooms. According to Lodging Econometrics, the number of projects in the pipeline increased 38 percent in 2012. Although starts are expected to slow in 2013, there are 341,204 rooms currently in the pipeline. The “pipeline mix,” according to Lodging Econometrics, shows “big increases for smaller projects Under Construction and a decline in larger Early Planning projects.” Smaller projects enter the pipeline faster. “At year-end, Luxury, Upper Upscale and Casino projects totaled just 7 percent of all projects in the Pipeline, while Upscale and Upper Midscale accounted for a whopping 76 percent. Ninety-one percent of all Pipeline projects are less than 200 rooms.” (“United States Lodging real estate trends”-executive summary, Winter 2013, Lodging Econometrics)

Trends: • Hotel developers will renovate before building new properties. • As the economy continues to improve, business and vacation travelers are taking to the roads and airways, but this will be a slow transition. • International travel is still steady due to the weak dollar. • Occupancy rates are on the rise. • Green building is more commonplace in remodels and retrofits.

Drivers: • Occupancy rate • RevPar • Average daily rate • Room starts

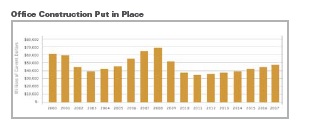

Office

Office construction is finally showing a solid but slow turnaround with 5 percent growth in 2012 and another 5 percent increase expected in 2013. High unemployment rates and sharp downsizing in the financial sector took its toll on office vacancy rates since the recession. Now, companies enjoying higher profits are again looking at growth and expansion. New office space is being absorbed at a faster rate, thus allowing for increased rents. According to the National Association of Realtors, “Office rents should increase 2.6 percent in 2013 and 2.8 percent next year, following a 2.0 percent gain in 2012.”

Trends: • The National Association of Realtors reports, “Vacancy rates in the office sector are forecast to fall from a projected 16.0 percent in the first quarter to 15.6 percent in the first quarter of 2014.” • Asking rents increased 0.8 percent to an average $28.46 per square foot, according to Reis.

Drivers: • Office vacancy rate • Unemployment rate

Commercial

Commercial construction is the third largest nonresidential construction market behind education construction and manufacturing construction. That’s why it is good to see that it continues into its third year of good growth, moving up 8 percent in 2012 and looking for another 7 percent to reach $50.3 billion in 2013. The slow rebound is coordinated with the return of consumer confidence and disposable income. The U.S. Census Bureau reported in March “Total sales for the December 2012 through February 2013 period were up 4.5 percent (±0.5 percent) from the same period a year ago.”

Trends: • According to the Department of Commerce, “[A]dvance estimates of U.S. retail and food services sales for February, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $421.4 billion, an increase of 1.1 percent (±0.5 percent) from the previous month and 4.6 percent (±0.7 percent) above February 2012.”

• “Nonstore retailers were up 15.7 percent (±2.3 percent) from February 2012, and auto and other motor vehicle dealers were up 8.8 percent (±2.3 percent) from last year.” • Consumer confidence was down in March 59.7 from 68.0 in February. (The Conference Board) • Expect more rethinking of commercial construction space to accommodate smaller stores and to combine in-store sales with online shopping. • Increased store remodeling could stall new construction. • Look for increasing multiuse projects.

Drivers: • Retail sales • CPI • Unemployment rate • Income • Housing starts • Building permits

Health Care

Health care construction was moderate in 2012, growing only 3 percent, but we expect it to pick up in 2013 to 8 percent to $44.2 billion construction put in place for the year. Demographics continue to drive our forecast, and baby boomers are retiring in larger numbers and more likely to need greater health care. However, there is a larger elephant in the room that makes prediction a bit dicey right now. The Affordable Healthcare Act, Obamacare, is set to provide access to affordable health insurance for millions of Americans who are currently uninsured. This looks like a potentially sudden shock to the system, even though it has been coming for three years now, because many have ignored it or tried to legislate it away. The “2013 CFO Outlook, Survey of U.S. Senior Financial Executives” by Bank of America/ Merrill-Lynch cites 58 percent of CFOs as seeing rising healthcare costs as a chief concern. That response isn’t based solely on the coming changes due to Obamacare, but also the concern for the continually rising health care costs that Obamacare seeks to improve. Meantime, health care providers will continue to focus on reducing costs for new facilities through use of technology and fewer frills.

Trends:

• Hospital beds per 1,000 people trending downward • Shorter patient stays • Increasing use of growing number of ambulatory-care facilities • Heath care industry still not prepared for increased number of insured starting in 2014 • Trend toward rebuilding existing facilities to use modern hospital design and allow for greater use of technology • Nontraditional funding sources for private nonprofit facilities. • Private development and equity. • Government or government-backed. • Pension and life insurance companies.

Drivers:

• Population change younger than age 18 • Population change ages 18-24 • Stock market • Government spending • Nonresidential structure investment

Educational

Construction for schools will pick up slightly in 2013 to 3 percent over 2012 levels at an annual rate for construction put in place of $87.2 billion. The increases in residential construction and tax revenues for states and municipalities will help bring this market back in many areas of the country. At the same time, states and communities with decreasing populations, due to people moving to find better jobs, continue to try to consolidate older, underutilized schools. Private schools may continue to suffer as parents facing tight budgets avoid the higher costs. For higher education, students are becoming more discerning about their return on investment and taking a closer look at the growing number of degree programs offered online.

Trends: • Significantly less funding from states for K-12 schools. • Enrollment growth 2.5 million in the next four years. • New school designs more flexible for changing classrooms and greater use of natural light. • Greater attention to reducing energy use and employing green building technologies. • Harvard installs 600-kilowatt solar array. • Greater focus on safe schools after recent horrific shootings on campus.

Drivers: • Population change younger than age 18 • Population change ages 18-24 • Stock market • Government spending • Nonresidential structure investment

Religious

After nine years of being in a shrinking market, religious construction is set to grow 2 percent in 2013 to $3.9 billion. Much of this growth is likely to be renovation as newly formed congregations move into vacated retail space or reoccupy church buildings abandoned by other faiths. As the housing market slowly continues a growth trend in the coming years, we may also see more expendable income for contributing to new community houses of worship.

Trends:

• The lending environment continues to be a challenge for many congregations. • Establishing a capital campaign is becoming increasingly common. • Many churches are seeing tremendous declines in contributions and tithes. • More parishioners are relying on their houses of worship to provide guidance and assistance, further stretching thin resources. • New methods for charitable giving, including online giving and donation collections, are empowering religious organizations. • Improved space utilization and additions are taking the forefront, as new construction is increasingly not an option. • Churches are becoming smarter about attracting parishioners who are drawn in by facilities and the church building itself. • Energy efficiency, green sustainability and long-lasting quality are becoming top features many congregations want in worship houses.

Drivers:

• GDP (slowing) • Population • Income • Personal savings rate

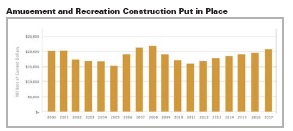

Amusement and Recreation

Our forecast calls for a modest increase of 3 percent for 2013 in amusement and recreation construction markets. There are a few large projects on the horizon, like the new Vikings stadium and the proposed domed stadium on the campus of UNLV, but lack of funding and support across the country will keep growth down in the near term until another round of renewal and venue competition starts in a few years. The casino and gambling industry has been hit hard since the recession, but some properties may begin to work their way out of financial difficulties and either be completed or shut down.

Trends:

• The San Francisco 49ers have recently broken ground on its new

$850 million stadium. • Minnesota Vikings $1.1 billion project has been approved by the state senate. • Casino plans are under way in a number of states, including New York, Pennsylvania, Maryland, Florida and Ohio, with some investors coming from offshore. • Public/private venture planned for the campus of UNLV includes a 50,000-seat domed stadium but still waiting approvals and taxpayer votes on plan to allow the project to be tax-free. • Competition in the gaming sector will draw business away from some existing gambling centers, such as Atlantic City, as well as other public arenas.

Drivers:

• Income up (slightly up) • Personal savings rate • Unemployment rate

Transportation

Transportation construction grew 8 percent in 2012 and will continue to show relative strength in 2013, growing another 8 percent to $39.6 billion dollars. With the passage of MAP-21 and the expanded federal Transportation Infrastructure Finance and Innovation Act (TIFIA) loan program, the transportation market finally has some degree of certainty for its funding in the near term. According to a new report by the American Road and Transportation Builders Association, (ARTBA), the “U.S. Transportation Construction Market Forecast 2013” calls for sluggish growth in highway and bridge construction due to reduced federal and state budgets, but rail-especially private freight lines-and ports will continue a slow expansion in the forecast period through 2017.

Trends:

• According to the American Association of Railroads, “Excluding coal, U.S. carloads were up 3.4 percent (22,121 carloads) in September 2012, their biggest percentage increase in four months and their 34th straight year-over-year monthly increase.” (Rail Time Indicators, Association of American Railroads, October 5, 2012) • The FAA Modernization and Reform Act will provide $63.6 billion for the agency’s programs between 2012 and 2015. • By 2021, more than one billion people a year will take to the air. • High-speed rail is slow to get projects off the ground due to state funding and political resistance. • Growth in container ports is recovering from the recession. • Intermodal transportation will be the focus of new projects.

Drivers:

• Population • Government spending • Transportation funding

Communication

After a 2 percent drop in 2012, communication construction will start a steady comeback in 2013, with construction CPIP up 4 percent to $17.8 billion and growing 6 to 7 percent through 2017. As data centers continue to proliferate, there has been more attention on their insatiable need for energy. That will stimulate more energy-conscious faculties in the future. Communications security, especially over the Web, is a growing concern for businesses as well as for government, with the focus being on an increasing likelihood of attacks by terrorists and foreign governments. While one might think we are approaching market saturation for smart phones and wireless communications, the market keeps going up as more consumers hook up several devices and look for constant, high-speed connectivity.

Trends:

• “Mini towers” for increasing coverage and spectrum will increase rapidly in the next five years. • Wireless technology is fastest area for growth as telecoms roll out more 4G technology with smartphones and tablets. • Data security is critical for large businesses and governments in the face of potential disasters and threats from hackers and foreign enemies.

Drivers:

• Innovation/technology • Global mobility • Population • Security/regulatory standards • Private investment

Manufacturing

Manufacturing construction increased 17 percent in 2012 and will continue with another 6 percent for 2013 through 2014. Due to reduction in energy costs in the U.S. relative to other countries around the globe and the increase in transportation costs, manufacturing will continue to reconsider operations in the U.S. or returning to the U.S. The resurgence of the automotive industry is a big boost to manufacturing as is the continuing exploration and mining for shale oil and gas.

Trends:

• “New orders for manufactured durable goods in February increased $12.4 billion or 5.7 percent to $232.1 billion. … This increase, up five of the last six months, followed a 3.8 percent January decrease. Excluding transportation, new orders decreased 0.5 percent. Excluding defense, new orders increased 4.5 percent.”

(U.S. Department of Commerce, March 26, 2013) • “Capacity utilization rate for total industry increased to 79.6 percent, a rate that is 0.6 percentage point below its long-run (1972-2012) average. September output of durable goods dropped 1.7 percent.”

(Board of Governors, Federal Reserve, March 15, 2013) • “Reshoring of manufacturing” is happening slowly, in part due to availability of lower energy costs.

Drivers: • PMI • Industrial production (slightly up) • Capacity utilization (slightly up) • Factory orders • Durable goods orders • Manufacturing inventories (slightly up)

J. Randall (Randy) Giggard is managing director of research services for FMI, Raleigh, N.C. He is responsible for design, management and performance of primary and secondary market research projects and related research activities, including economic analysis and modeling, construction market forecasting and database management. Giggard’s particular expertise is in the areas of market sizing and modeling, competitive analysis, sales and market performance evaluations, buying practices and trends analysis.

FMI is the largest provider of management consulting, investment banking and research to the engineering and construction industry. FMI provides clients with value-added business solutions, including Strategic Advisory, Market Research and Business Development, Leadership and Talent Development, Project and Process Improvement, Mergers, Acquisitions and Financial Consulting, Compensation Benchmarking and Consulting and Risk Management Consulting.

Reprinted by permission from FMI. To read the entire report, go to www.fminet.com